"We're seeing a trend of van insurance prices rising for many. It's something we've also seen across car and home insurance too. That's why it's more important than ever to not accept your renewal offer without first shopping around with a site like Confused.com.

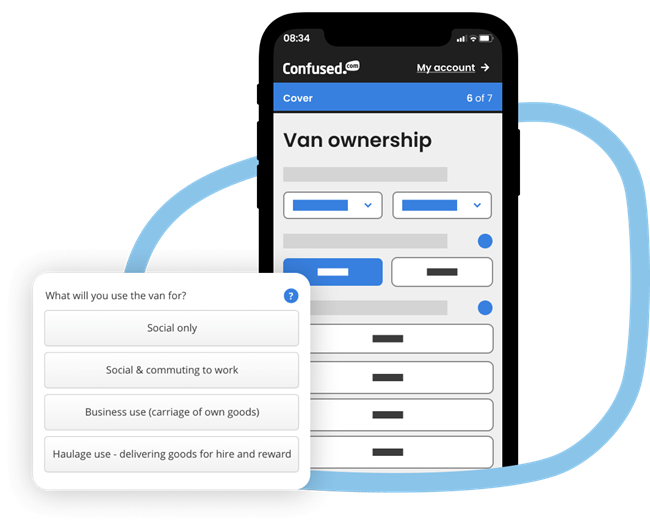

To help save further money, make sure you get the right cover for how you use your van. Some business van insurance policies will only cover the vehicle if it's stolen and not the tools inside. The cost of replacing these could be covered by adding-on tool insurance onto your policy."