Key takeaways

In 2025, the average monthly life insurance premium in the UK is £27 according to Confused.com data*. Crucially, the younger you buy a life insurance policy, the cheaper your premium is likely to be on average.

The monthly cost of a single life insurance policy for those aged 18-24 in 2025 is £12 on average, this is the cheapest price of any age group. On the other end of the scale, those aged 55+ face the most expensive monthly single life insurance premiums on average, paying £48.

*These figures are courtesy of a report conducted by Confused.com to analyse life insurance premiums in the UK. Other key takeaways include:

- Average annual premium in the UK is £324 in 2025

- Average ‘sum assured’ in the UK is £168,318

- In 2025, only 20% of life insurance policies include critical illness cover

How much cover are people opting for?

When it comes to life insurance, ‘sum assured’ is the agreed pay out amount at the end of the policy or when the policyholder dies. This amount is guaranteed and paid to the policyholder or the nominated person(s), but typically, the greater the sum assured, the higher the monthly or annual premium is.

In 2025, the average sum assured in a life insurance policy is £168,318. This figure has slightly fluctuated over the past 5 years with an average of £175,570. While your sum assured is a pre-agreed amount, you can usually change this during a policy to suit your needs. It’s always important to accurately estimate the sum assured as this is the amount that is paid out to your family or beneficiaries. This can be used to cover debts, funeral costs or large payments, such as a mortgage, for example.

Is there a gender gap?

There’s a definitive gender gap in terms of sum assured in a life insurance policy over the past 5 years. From 2020-2025, the average sum assured for women in a life insurance policy is £164,032. For men, this rises to £187,466 over the same time period, on average.

There are several reasons behind this, one being the gender pay gap. Women are also statistically likelier to take on the stay at home parent role than men. Because of this, men typically insure against a higher sum.

Is there a difference between age groups?

When it comes to age groups, 25-34 year olds have the highest average sum assured at £228,361 over the past five years. On the other side of the coin, those aged 55+ insured against the lowest sum assured with an average of £81,910. Having said that, the 55+ age group saw the biggest rise of average sum assured between 2020-2025 at 23%. The average sum assured for those aged 18-24 actually decreased by 8% over the same period.

So why are younger life insurance policyholders likelier to insure against a larger assured sum? Typically the younger you are, the cheaper a life insurance policy is. As such, it’s generally more attractive and cost effective to insure against a larger sum, particularly compared to older age groups.

How to calculate your cover amount

There are a range of factors you should take into consideration when determining your sum assured amount. The decided amount should take into account your family’s needs and your financial situation, along with other factors, including:

- Your age

- How many children you have

- The property you own

- Any financial responsibilities (including outstanding mortgages or debts)

- Typical income

- Medical history

Considering each factor, you can build up a good idea of your ideal cover amount and assured sum. This can help ensure you’re getting sufficient cover without paying for more than you actually need.

This is slightly different to ‘sum insured’, which refers to overall guaranteed and non-guaranteed cover available when a life insurance policy is bought.

Try our life insurance calculator to work out how much life cover you need.

The cost of life insurance is calculated through several key factors. Despite that, there are clear differences in average monthly and annual premiums between age groups and gender.

While your age and gender can impact what you pay, your premium may be cheaper or more expensive compared to the average amount of someone with a similar profile.

That’s because your medical history, financial commitments and living situation are considered in addition to other factors.

An insurer will assess all of your personal circumstances to present you with a bespoke quote based on your situation.

The average cost of a life insurance policy is £27 a month or £324 a year.

Both of these amounts have risen by 9% since 2020.

How age impacts the cost of life insurance

Generally, life insurance premiums tend to be cheaper the younger you are.

For example, in 2025, the average cost of a life insurance policy for those aged 18-24 is £12 monthly, or £141 annually. These figures gradually rise concurrently with age groups. The oldest age group (55+) face the highest life insurance premiums in 2025 of £48 monthly, or £573.

Younger age groups (18-24, 25-34 and 35-44), have all seen reduced annual premiums over the last five years, with cost reductions of -5%, -12% and -6% respectively. But the 45-54 and 55+ age groups have actually seen cost increases since 2020 - 13% and 38% respectively.

| Age | Monthly average premium between 2020-2025 | Annual average premium between 2020-2025 | |

|---|---|---|---|

|

Group 1

|

18-24

|

£11.52

|

£138.25

|

| Trend change: | |||

|

Trend Change:

|

-5%

|

||

|

Group 2

|

25-34

|

£18.48

|

£221.75

|

| Trend Change: | |||

|

Trend Change:

|

-12%

|

||

|

Group 3

|

34-44

|

£26.65

|

£319.75

|

|

Trend Change:

|

-12%

|

||

| Trend Change: | |||

|

Group 4

|

45-54

|

£32.39

|

£388.68

|

| Trend Change: | |||

|

Trend Change:

|

-6%

|

||

|

Group 5

|

55+

|

£38.68

|

£464.24

|

| Trend change: | |||

|

Trend Change:

|

38%

|

||

How gender impacts the cost of life insurance

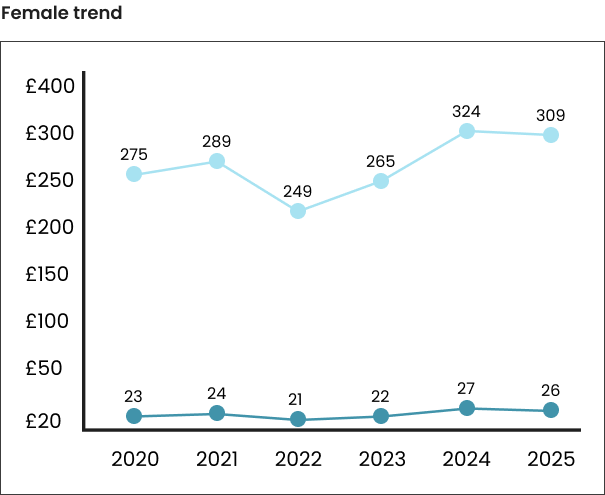

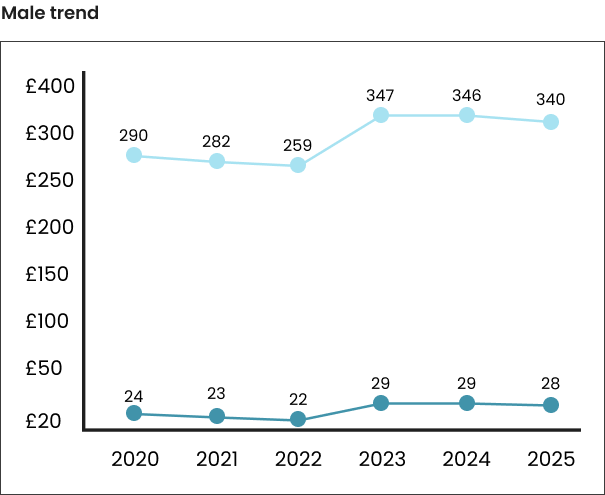

When it comes to gender, men typically pay more for life insurance than women. In 2025, women are paying £309 on average annually and £26 monthly. This is a 12% increase since 2020. Men on the other hand pay £340 annually and £28 monthly on average in 2025, this is a 17% increase since 2020. So, why do men tend to pay more for life insurance than women? The EU Gender Directive, introduced in 2012, actually prohibited insurance companies from basing premiums on gender. However, men have a shorter life expectancy on average and are likelier to work in riskier occupations.

How many people are opting for critical illness cover in their life insurance policies?

Critical illness cover can provide you with a lump sum if you develop a condition during a life insurance policy, pending you have this type of cover in place. The terms of the cover is typically stated when you buy a policy and included in the relevant documents.

Usually, an insurer will provide a list of conditions that are covered, you should be aware of this before buying a life insurance policy. Some life insurance providers pay out upon diagnosis, others may state that a condition has to have progressed, or that specific treatment has been administered.

In 2025, only 20% of life insurance policies included critical illness cover, but this has increased by 11% compared to 2020. Over the past 5 years men (8%) are more likely to include critical illness cover in a life insurance policy than women (6%).

In 2020, just 2% of life insurance policies owned by women included critical illness cover, this increased to 20% in 2025. There’s no definitive reason why more women are choosing critical illness cover, however the amount of women aged 16-64 in employment has risen gradually since 1971. Greater financial protection could be one reason why more and more women are choosing to include critical illness cover in life insurance policies.

For men, 19% of life insurance policies included this type of cover in 2020, this dropped to 16% in 2025. However this decreased significantly between 2021 and 2024. In 2021, the number of life insurance policies owned by men that included critical illness cover decreased to just 1%. In 2022, 2023 and 2024, critical illness cover was included in male life insurance policies just 1%, 1% and 10% respectively before rising again in 2025.

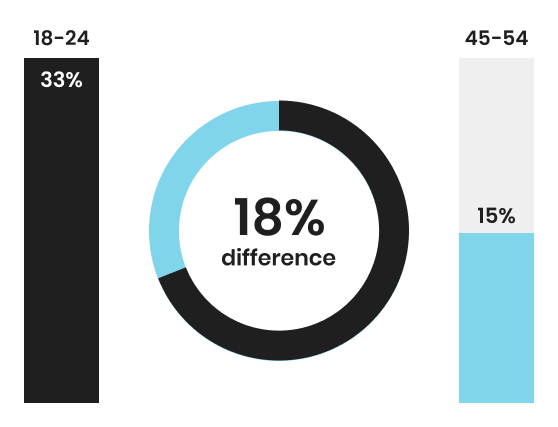

When broken down by age demographics, younger age groups are more likely to opt for critical illness cover. In fact, 18-24 year-olds lead the way with 10% of the age group choosing to include this type of cover in their life insurance policy over the past 5 years, on average. Only 5% of those aged 45-54 included critical illness cover in their policy over the same period, on average.

Joint/single policies

As you’d imagine, a joint life insurance policy covers two people as opposed to one. The key difference being that a pay out for a single life insurance policy typically occurs after the policyholder has died.

This is different to a joint policy where a specified amount of cover is paid out if the first person dies, during the length of the policy. Once this amount is paid out, the policy usually ends. This means the surviving partner no longer has cover under this policy.

You don’t actually need to be married to consider a joint life insurance policy. However, this type of policy is convenient for those sharing financial commitments, so it tends to be a popular policy among couples.

Key to a joint policy is that both policy holders receive the same level of cover. So, if either individual has different protection requirements, a joint life insurance policy may leave one individual with too much or not enough cover.

In 2025, a single life insurance policy costs £28, whereas a joint life insurance policy costs £26, on average. Since 2020, a single life insurance policy is costlier than a joint policy, so for couples, it’s a cheaper option to consider.

Between 2020-2024, single life insurance policies were preferred (74%) over joint policies, on average. However, in 2025, those opting for a single policy dropped to 63%. Over the past five years, joint policies are becoming more popular. In 2025, 44% of men are choosing a joint policy, whereas only 33% are doing the same, on average.

What are the different types of life insurance?

Critical illness cover

Pays out a lump sum if you're diagnosed with an illness covered by your policy

Mortgage life insurance

Life insurance with a pay out that reduces in line with your mortgage balance.

Joint life insurance

Covers 2 people under 1 policy, with 1 premium to pay and 1 pay out when either of you die during the policy term.

Health insurance

Covers the cost of private medical care, helping you avoid NHS waiting lists to get the cover you need, quickly

Income protection insurance

Pays out a percentage of your income if you can't work due to illness or injury.

Need more help?

How do I get a quote?

You can compare life insurance quotes through price comparison websites like Confused.com. We'll use the details you provide us with to help you find the right cover for your needs.

To help you answer our questions correctly, we'll guide you through the process with helpful tips and extra information along the way.

What is life insurance?

Life insurance offers cover that can pay out a lump sum if you die, or if you’re diagnosed with a specified condition depending on the policy.

This can provide your family or other dependents with financial support after you die or suffer from an illness covered by a life insurance policy.

When should I get life insurance?

The younger you are, the cheaper life insurance premiums tend to be. So it’s worth considering buying life insurance early, especially as you’ll pay a lower premium for the duration of the policy.

It’s fairly common for people to consider life insurance around major life events. If you’re getting married, buying a home or having children, having cover in place can ensure your family and dependents are financially protected.

Do I need life insurance?

It’s always worth assessing your personal circumstances and asking whether you’d like to provide financial protection for your family. If you have key financial commitments such as a mortgage, for example, a life insurance pay out can help pay off any outstanding debts.

Consider whether your family may need a financial safety net should the worst happen. You can then look at the different types of life insurance to decide what policy suits your specific needs.

What types of life insurance are there?

The two main types of life insurance are term life and whole of life insurance. You can get increasing, decreasing or level term life insurance.The amount of cover these policies offer can fluctuate over a fixed term depending on the life insurance you buy.

Whole of life insurance is different as it doesn’t include an end date and lasts for an entire lifetime. As long as you keep up your premium payments, a lump sum will be paid out to your beneficiaries when you die.

There are other variations of life insurance such as a joint policy (useful for couples), income protection, over 50’s life insurance and mortgage life insurance. These policies are tailored and can provide additional benefits based on your requirements.

You can also add critical illness cover to your life insurance policy. It comes at an extra cost but you’ll have to option to make an early claim on your policy if you're diagnosed with a condition stated in your policy.